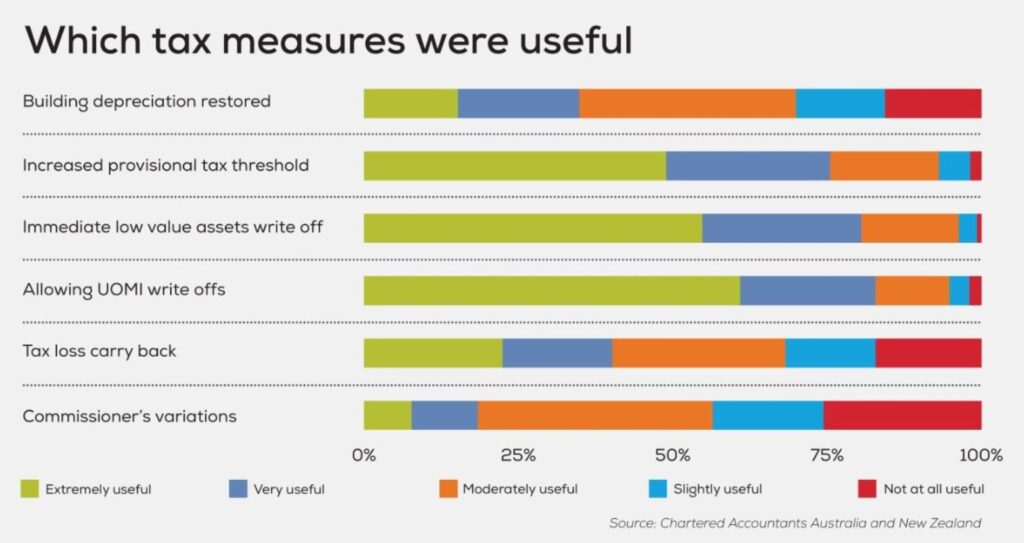

Increased provisional tax thresholds, immediate low-value asset write offs and allowing the deferral of tax payments and use of money interest (UOMI) write offs were the most popular tax measures introduced by the Government to help businesses survive COVID-19.

A survey of Chartered Accountants and Tax Management NZ clients held late last year has provided the first deep dive into which COVID-19 tax measures worked, and which didn’t. Most did.

Eighty three percent of respondents rated UOMI write offs as extremely or very useful for their clients, 81 percent similarly rated low-value asset write offs and 75 percent for increased provisional tax thresholds.

“Remembering what the Government and Inland Revenue were confronted with back in March last year, including having to act fast and not knowing for sure what would work, the survey indicates the Government’s business response is as deserving of accolades as its health response,” says John Cuthbertson, New Zealand Tax leader for Chartered Accountants Australia and New Zealand.

“The Government took a shot-gun approach to business tax relief and a very high percentage was on target.”

When it came to rating IR’s services, 63% of respondents said IR’s helpfulness was excellent or good, for responsiveness it was 59%, understanding of the issue (57%) and consistency (51%). At worst, only 15 percent said services were poor or terrible.

“In the circumstances, these levels of positive feedback are remarkable,” said Cuthbertson. As an example of what IR was confronted with, in less than a month it received more than 77,000 Small Business Cashflow Loan Scheme applications and approved loans worth approximately $1.2 billion.

Not all tax measures rated highly, though some problems related to timing. Less useful measures were tax loss carry back provisions (only 40% support as extremely or very useful), the restoration of building depreciation (35%) and the IR Commissioner’s variations such as an extended deadline for filing statements for R & D loss tax credits and extended time for tax pooling transfers (just 19%). More than a quarter of respondents rated the variations as not useful at all.

An example of a timing problem is the building depreciation measure which will support recovery and will benefit commercial building owners long term. “It’s just that this timeframe was not front of mind for survey respondents given that the 2021 income year was not yet complete.

“The measure eventually will reduce income tax payable.”

A temporary tax loss carry-back scheme was introduced early last year in response to calls from CAANZ and pandemic-hit businesses and a permanent measure has been signalled by the Government.

Cuthbertson said the temporary measure failed for two reasons: “Firstly, the timing was all wrong. COVID-19 hit New Zealand at the end of the financial year for most taxpayers, and after the summer season for our tourism dependent sectors.

“In short, many taxpayers wouldn’t have had losses to carry back.

“Secondly, respondents stressed the risk of estimating future tax positions in what has been an unusually uncertain time and the complexity of the rules.”

Cuthbertson said while these factors were significant, they were largely beyond the control of policy makers.

“The policy makers need to have a pragmatic look at the realities for many small businesses including shareholder distributions, meaning there are no losses left in the business to carry-back.”